2021 has been a busy year for fintech. While several sectors floundered in the pandemic environment, for many fintech companies, COVID-19 acted as a catalyst, accelerating the shift towards digital from both consumers and businesses. VCs, private equity firms, and even institutional investors have been quick to jump in on the opportunity; the global fintech funding more than doubled to reach $131.5 billion, recording a 168% increase from 2020. As the momentum continues and the industry delivers exponential growth, we examine the top fintech trends in 2022.

1. The explosion of embedded finance solutions

Embedded finance is likely to go mainstream in 2022. Over the past year, more and more non-financial companies have been integrating financial solutions into their existing portfolio. For consumers, this means getting access to financial services directly from the platform itself; an example is a taxi app with an inbuilt payment solution.

From payments to investments and lending, embedded solutions are penetrating every aspect of financial services. Last year saw the boom of Buy-now-Pay-later (BNPL) offerings from companies like PayPal and Klarna, offering customers easy installments while shopping online. This trend is well-positioned to grow exponentially as fintech and banks explore opportunities to become service providers to these non-financial companies.

2. The move towards autonomous finance

Integrating AI in finance is more than just a trend now. By using a set of preprogrammed criteria, AI solutions can automate repeated processes and drive efficiencies, thus enhancing user experience. More complex solutions are emerging with technological advancement as we see a shift towards autonomous finance. For example, there are systems for the automatic assessment of the best directions for investment, assistant systems for creditors and bankers, automating routine administrative tasks, and complex analytical ones. We expect more advanced autonomous financial solutions that revolve around self-driving funds to emerge this year.

3. Towards the era of decentralization

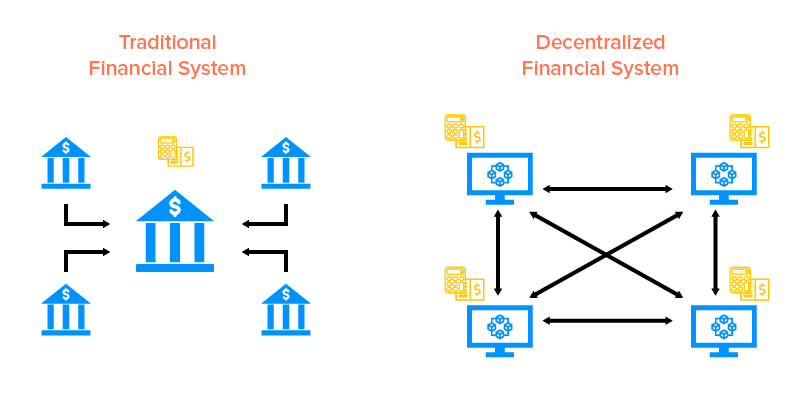

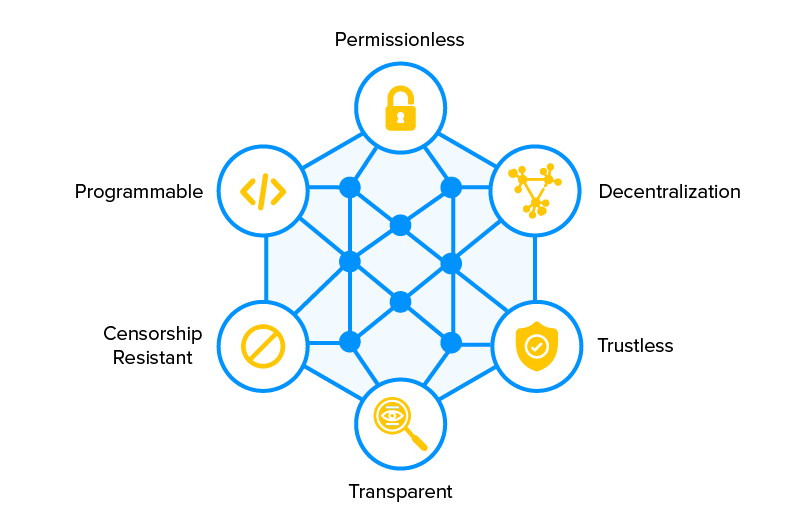

Decentralized Finance (DeFi) promises to create alternatives to financial services for anyone with access to a smartphone and internet connection. Built on distributed ledger technology, DeFi removes the need for intermediaries like banks, allowing financial transactions directly between users. The market has been booming with the rapid adoption of cryptocurrencies, tokenization, and non-fungible tokens (NFTs).

Components of a DeFi system

Last year saw massive traction with banks jumping the bandwagon and exploring blockchain and digital currencies opportunities. The growing popularity of cryptocurrencies has forced central banks across countries to investigate the possibilities of developing centrally backed digital currencies (CBDCs). In 2022, this momentum will continue as we see more mainstream adoption with financial institutions building more solutions around blockchain.

4. The race of the super apps will intensify

The most profound paradigm shift likely to emerge this year will come from the fintech aiming to provide a ‘one-stop-shop’ app or super-app. Such apps typically offer a different suite of products/services from a single platform, including booking appointments, hailing cabs, booking flights, shopping, food delivery, banking services, etc.

Eastern regions have already seen much success with apps like WeChat (China), and Alipay (China), super-apps in the West are yet to spark similar interest. But 2022 could see a significant transformation in that regard, as a handful of fintech firms across the US and Europe like Revolut and Block are looking to bring together a diverse range of services into a single application.

5. The regulatory dilemma

With the fintech space constantly evolving, regulatory bodies are trying to keep up with divergent approaches to manage risks. As cryptos and digital assets gain momentum, there are a variety of regulations coming into play worldwide to define guidelines around their ownership, distribution, and use. With the world going digital, regulators are taking an increasing and focused interest in data privacy.

In fact, newer, disruptive services like BNPL have been garnering attention from regulators. Even as BNPL users in the US reached 45 million in 2021, regulators raise concerns regarding the possible accumulation of huge debt, especially with exorbitant late fees if not paid on time.

Integration of technologies such as AI and IoT in financial services – while proving beneficial on many fronts – is largely also aiding to solve the regulatory crises. From identifying fraud signals to risk classification using Artificial Neural Networks (ANN) and compliance measurement, RegTech leverages advanced tech algorithms to mitigate risk and prevent financial crimes. With digital advancements comes the increased risk of fraudulent activities and cybercrime. To make customer protection a priority, regulations will become more stringent going forward. Systems like open banking will lead the way to a more open and transparent environment.

6. Climate first! The move to sustainable finance

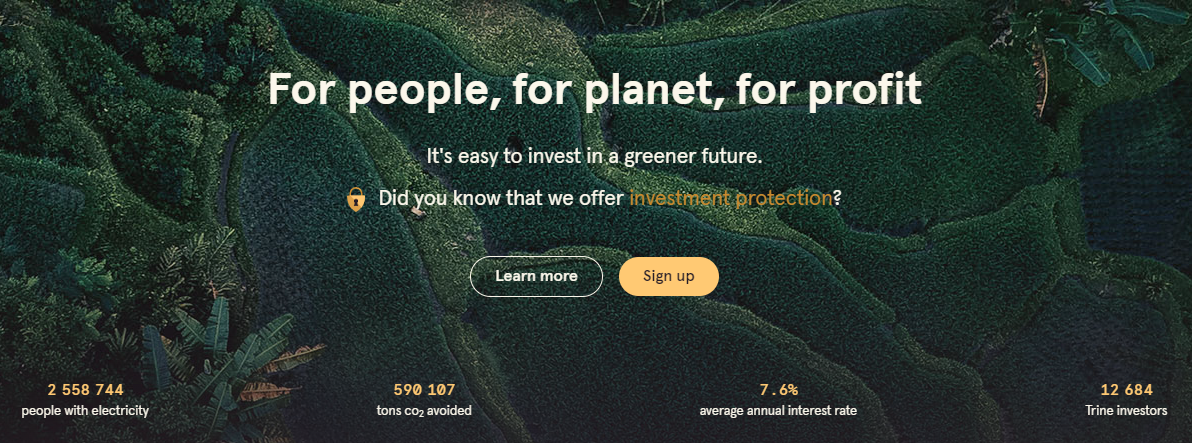

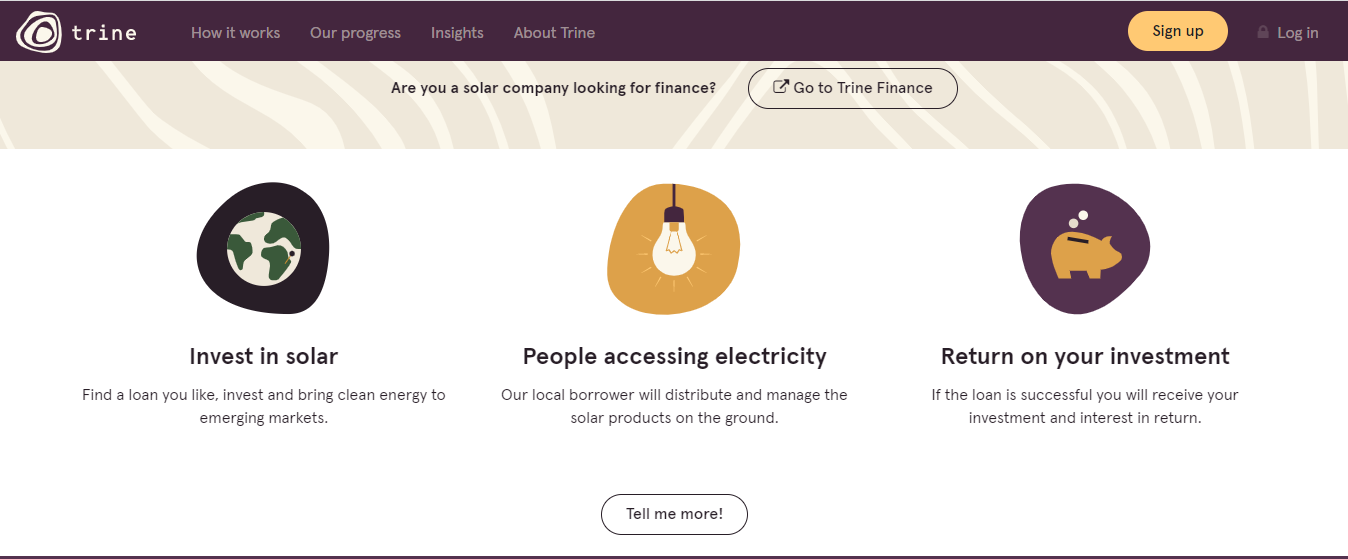

Given the conversations around sustainability and prioritization of ESG, we can expect fintechs to come up with ESG capabilities. With green fintech, technology retains a dual focus: sustainability and finance. With the banking sector actively seeking ways to adopt sustainable practices to reduce their carbon footprint and increasing investments in ESG, fintechs are actively catching up, if not faster. Finnish fintech firm Cooler Future recently launched an app that urges firms to make climate-friendly investments and track their impact. Similarly, Trine is a planet-first fintech firm urging investments in solar and other clean energies for emerging markets. Stripe Climate, a tool launched by payment giant Stripe, aims to redirect online business revenue towards reducing carbon footprints.

As the world wakes up to the rapid pace of climate change, fintechs will play an integral role in facilitating climate-first sustainability initiatives.

7. Collaboration, not competition is the way forward

Today, the focus has shifted from competition to collaboration. The future of financial services will be driven by partnerships between fintechs and banks. Tapping into the traditional legacy infrastructure, strict regulatory environment, and existing large customer base of banks leave room for fintech to innovate and come up with specialized solutions for customer segments. Cross River Bank and its fintech partner Affirm do just that.

Open banking is set to further drive this collaboration. In fact, a recent report indicates that the largest collaboration agreements in the fintech ecosystem in 2021 were related to open banking, followed by BNPL and sustainability investments. One such example arose in the open banking partnership between American Express and Tink last year. American Express now integrates Tink’s open banking technology into its risk analysis and application processes. As a result, customers save time and have a better experience. Going forward, fintech companies and traditional banks have multiple opportunities to explore to serve new demographics and emerging sectors.

8. Solutions for all

As the world goes digital, several parts of the population cannot afford high-speed internet to securely manage their financial needs. In fact, globally, over 1.7 billion adults remain unbanked. Fintechs can bring the world a step closer with accessible financial services. From SMEs to gig economies, financial inclusion has been a huge selling point of fintechs. These companies are increasingly coming up with unique propositions targeting specific segments. With the potential to lower costs and increase accessibility and speed, fintechs can democratize access to financial services that can be tailored at scale.

From mobile money to services like cross-border remittances and personal payments, fintechs are playing an important role in increasing the banked population around the world. For instance, with more than 50% of Latin America’s population non-funded and underbanked, the last two years have paved the way for a historic boom in fintechs in Latin America. With targeted demographics, highly personalized experiences, and digitally native infrastructures, especially in Brazil, Mexico, Argentina, and Colombia, fintechs have witnessed massive growth. Compared to traditional institutions, they’re able to quickly introduce affordable financial services and products to markets. Further, the community-focused approach undertaken is helping build a sense of belonging.

Today, the financial industry is driven by FinTech disruption. The next few years are only set to pave way for more partnerships and changes in the way the financial services sector operates.

To stay up to date with the latest trends, gain in-depth market insights on the financial services sector, and obtain customized insights for your organization, contact us today.

Based on insights by Shreerupa Banerjee, Manager- BFSI Intelligence, Netscribes.