Key highlights

- CATL is emerging as a dominant force, installing a substantial volume of EV batteries, reinforcing its significant market share.

- China and the US emerge as key drivers of EV battery demand, showcasing distinct trends in regional EV adoption.

- Anticipation of a battery price war signals intensified competition, driving down costs and potentially accelerating EV adoption rates.

- Despite economic uncertainties, falling lithium prices hold the promise of accelerating EV adoption rates, reshaping the automotive industry's landscape.

The electrification revolution is reshaping the automotive industry, placing the rapid advancement of electric vehicle (EV) batteries at the forefront. With the global demand for cleaner and more sustainable transportation solutions on the rise, the EV battery landscape is undergoing a significant transformation. In the upcoming sections, we will explore the expansive and evolving terrain of electric vehicle economics, mainly EV batteries, examining various facets including demand trends, technological advancements, and regional dynamics.

CATL’s Pivotal Role in Fulfilling the Demand for EV Batteries

In January 2024, global battery usage for EVs reached 51.5 GWh, marking a significant 60.6% increase from the 32.1 GWh recorded in the same month the previous year. Notably, CATL, the Chinese power battery giant, played a pivotal role in this surge, installing 20.5 GWh of batteries during January—a remarkable 88.1% increase compared to the 10.9 GWh installed during the same period last year. CATL’s dominance in the global market remained unchallenged, with the company maintaining a commanding 39.7% share, making it the sole battery provider with a market share exceeding 30%.

The Surge of Lithium Iron Phosphate Cathodes in Battery Chemistry

Within the battery chemical landscape, lithium iron phosphate (LFP) cathode chemistries experienced a remarkable surge, reaching their peak share in the past decade. This surge in popularity can be attributed to the preference of Chinese Original Equipment Manufacturers (OEMs) to lessen dependence on essential elements like nickel and cobalt, thereby enhancing cost-effectiveness. Despite their comparatively lower energy density, LFP batteries maintained affordability and garnered widespread commercial acceptance.

China and the United States Emerged as The Key Catalysts in Driving EV Battery Demand

Regionally, China and the United States have emerged as pivotal drivers of the demand for EV batteries. China’s surge in battery demand was bolstered by a substantial uptick in sales of economic electric cars towards the end of 2023, while the United States experienced significant growth in battery demand despite a comparatively more modest increase in EV sales. Notably, the average battery size for EV batteries in the US remained higher, underscoring manufacturers’ endeavors to provide longer all-electric driving ranges.

Electrification Initiatives Drive Surge in Lithium Demand, Sparking Price Volatility

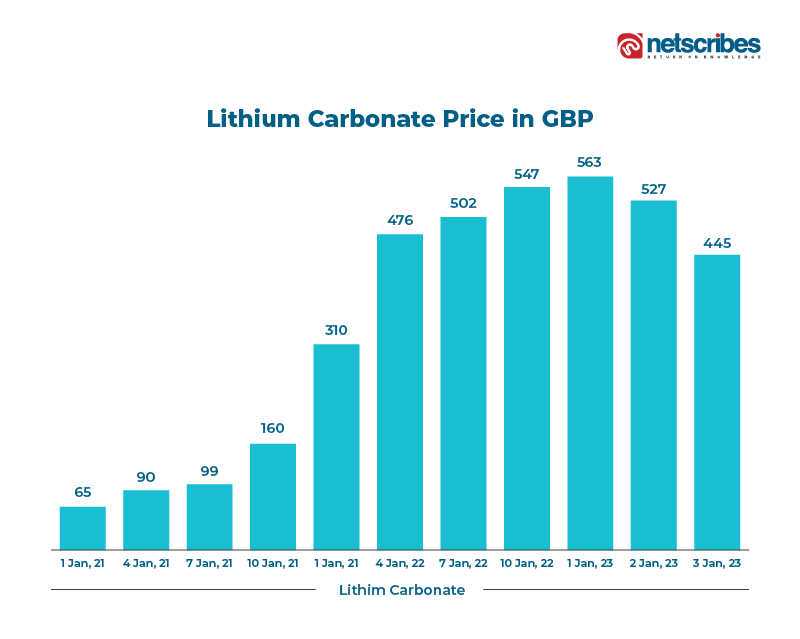

The surge in electrification initiatives has led to a notable rise in lithium demand. Economic electric car giants like Tesla are actively seeking resources due to the scarcity of lithium amidst the rapid expansion of EVs. This demand has caused lithium carbonate prices to skyrocket by over sixfold in recent years. However, in 2022, lithium prices experienced a significant downturn, undoing several years of consecutive increases. By November of that year, lithium carbonate prices in China reached an all-time high, only to collapse to a new low of 35–40% by March 2023, marking the end of the longest bull run in lithium’s history.

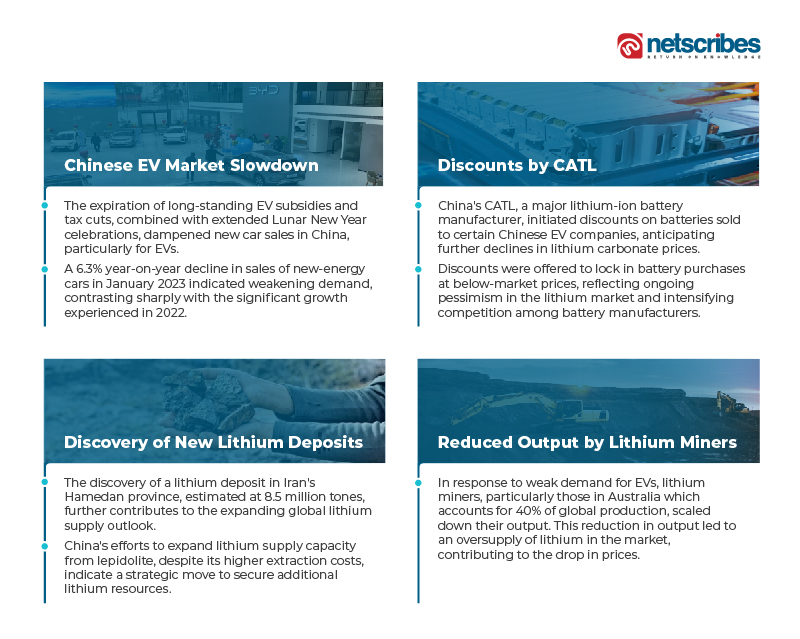

The following are some of the factors driving the decline in the price of lithium carbonate, particularly at the beginning of 2023.

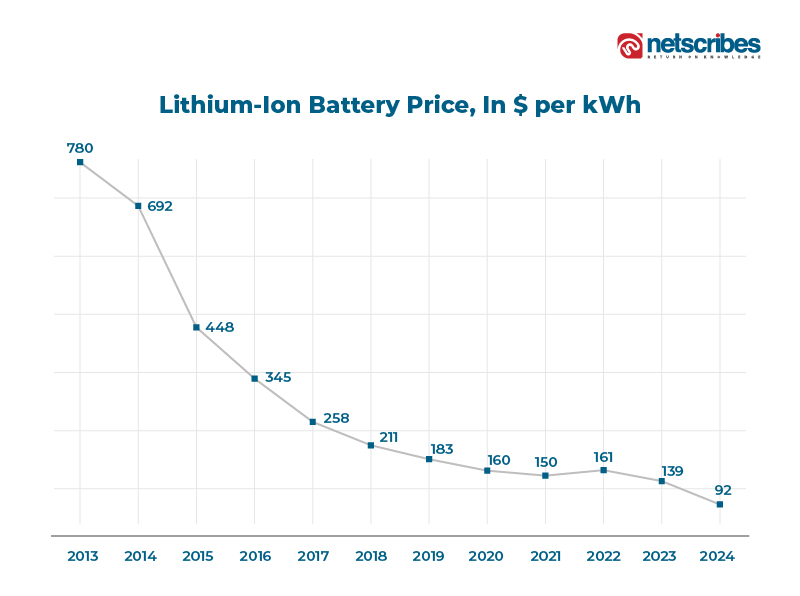

Lithium-Ion Battery Price Trends Over The Years

The anticipated surge in battery demand has fallen short of projections, largely attributed to concerns over a potential downturn in EV sales in China, a market representing over half of the global EV market share. Consequently, battery manufacturers have scaled back their demand for lithium. Concurrently, mining companies have ramped up lithium production in response to the sustained price escalation. Despite these shifts, battery prices are experiencing a downward trend, influenced by a variety of factors:

Global Supply Chain Enhancements and Price Reductions

The global supply chain has improved, resulting in greater production and lower prices. Governments across the world are aggressively encouraging the mining and cell manufacturing ecosystems with subsidies, which helps to reduce costs. As a result, there has been an oversupply of batteries in recent months, which coincided with a decline in demand, causing battery prices to drop.

Shift Towards EV Battery Storage Facilities

Governments worldwide are increasingly emphasizing the localization of storage facilities for EV batteries. These domestic and regional initiatives are playing a pivotal role in driving down battery prices, with potential long-term ramifications. For example, the provision of viability gap funding (VGF) for battery storage systems by the Indian government is projected to facilitate the establishment of approximately 4 gigawatts of battery storage capacity in India by fiscal year 2028, as assessed by the rating agency Crisil. Previously hindered by the prohibitive costs of batteries, India’s battery storage capacity is now primed for expansion, thanks to initiatives like the viability gap funding program.

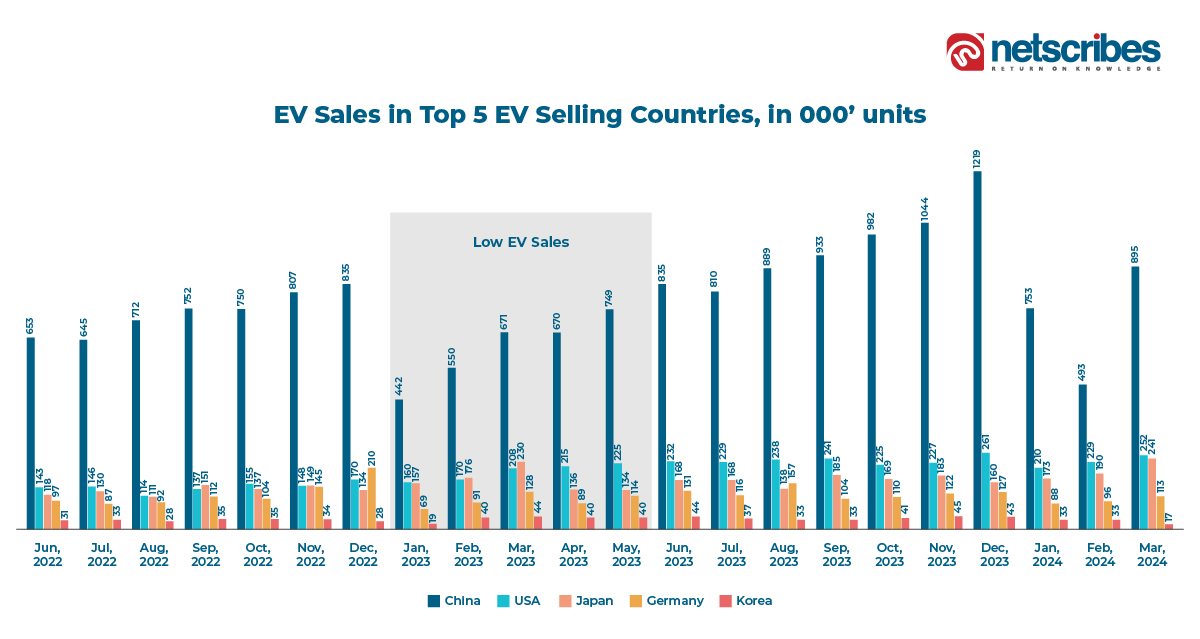

Fluctuations in Global EV Sales and Market Dynamics

The EV sales experienced a decline from January 2023 to April 2023, with China being significantly impacted. A similar downturn in EV sales was observed around the beginning of 2024, amidst weakened consumer demand in major economies such as China, the United States, Japan, Germany, and Korea. Tesla’s sales declined in the United States during this period, prompting many other automakers to follow suit by reducing prices. Moreover, incentive spending on EVs has surged over the past year, indicating a decline in demand, which in turn is lowering the EV battery prices, impacting the electric vehicle economics.

Conversely, China’s EV sales growth in the first quarter of 2024 was the weakest in a year. Sales of electric passenger vehicles in China increased by 10.5% in March compared to the same month a year ago, as automakers, led by popular BYD, offered deeper discounts and financing options to spur sales. According to data from the China Passenger Car Association (CPCA), sales of 1.03 million EVs increased by 14.7% year-on-year in January-March, marking the weakest quarterly growth since the second quarter of 2023. Authorities have collaborated with automotive manufacturers to incentivize customers to purchase vehicles and stimulate a stagnant economy. Initiatives include modifying vehicle loans to encourage auto trade-ins and eliminating government-mandated minimum down payments for new car purchases.

The Impact of Declining Lithium Prices on the Global EV and the Battery Market

Opportunities for Global EV Manufacturers

The current decline in lithium prices holds promising implications for EV manufacturers worldwide. Reduced lithium costs offer manufacturers the opportunity to streamline manufacturing expenses, potentially enabling them to provide consumers with more competitively priced EVs and energy storage systems. This trend aligns with the broader goal of making sustainable transportation and energy solutions more accessible to a wider customer base.

Possible Battery Price War

Industry analysts anticipate a battery price war that could significantly reduce the costs of EVs. CATL, the world’s largest EV battery manufacturer, intends to halve battery costs, intensifying competition with BYD’s affiliate, FinDreams. Given that EVs are primarily expensive due to their batteries, this competition is expected to enhance the competitiveness of EVs compared to conventional vehicles. CATL’s ambitious goal of slashing battery prices by 50% has prompted a response from FinDreams, further fueling competitiveness. By February 2024, battery costs per kWh had plummeted from 110 to 51 euros, underscoring the effectiveness of these initiatives.

This development coincides with a drop in EV demand in 2023, resulting in CATL’s first earnings decline in over two years. However, both CATL and BYD remain focused on cost reduction and technological advancements, with a particular emphasis on cobalt-free EV batteries to address ethical concerns. Efforts to expand the lithium supply and improve accessibility continue to drive ongoing cost reductions. China’s leadership in cobalt-free batteries reflects this trend, despite fluctuations in lithium costs, highlighting the industry’s commitment to affordability and sustainability.

Fueling Accessibility and EV Adoption

The drop in lithium prices is democratizing access to EVs and making them more accessible to a wider populace. This increased accessibility may spark a rise in EV adoption rates, resulting in significant development in the electric transportation and energy storage market.

Rising Challenges for Lithium Producers

Despite the potential benefits for the manufacturers of electric cars, falling lithium prices present substantial problems for producers and mining companies. These stakeholders are dealing with declining profit margins and need a strategic revaluation of their methods of production to effectively survive the current market volatility.

Supply Chain Resilience and Adaptive Strategies

Lithium price fluctuations resonate across the EV and battery supply chain, impacting long-term planning and investment objectives. This highlights the need for strong supply chain management methods and adaptive company models to minimize the effects of market volatility.

Stimulating Innovation in EV Battery Technology

The drop in lithium prices acts as a catalyst for innovation in the EV battery business, encouraging research and development efforts focused on diversifying battery chemistries and materials. Such innovation is crucial for increasing supply chain resilience and achieving long-term development in the face of shifting electric vehicle economics.

What Future Ramifications May Arise from the Current Lithium Price Landscape?

Despite continued growth, EV sales in 2024 are projected to grow at a slower rate than in previous years, with a year-on-year growth rate of less than 36% from 2022 to 2023.

Economic worries, notably high-interest rates, are projected to weaken consumer confidence, particularly in economies such as the United States, where financing is an important factor in car sales. The reduction of EV production projections by major Western automakers, along with underperformance in EV sales relative to expectations in Europe and the United States, may result in more delays or slowdowns in EV plant ramp-up in 2024.

Lithium supply is expected to expand in 2024, owing to expansions and greenfield projects launched in recent years. However, the present price situation may have an impact on supply dynamics, with some manufacturers considering reducing production or deferring growth. Despite the increase in domestic lepidolite and African spodumene projects in China, new capacity is projected to have start-up delays, adding to supply-side vulnerabilities. Market players anticipate rather moderate downstream lithium demand, resulting in a somewhat balanced market in 2024.

Looking ahead, the democratization EV access fueled by falling lithium prices holds the promise of accelerating EV adoption rates, fostering innovation, and reshaping the electric vehicle economics. However, economic uncertainties and supply dynamics may temper growth projections in the near term, underscoring the need for resilient supply chains and strategic foresight.

Explore how Netscribes’ Automotive and Mobility Solutions can help you navigate the evolving landscape of EV batteries and electric vehicle economics. Contact us today.

FAQs

Lithium prices are falling due to factors such as oversupply, reduced demand projections, and improvements in mining and production capabilities.

Falling lithium prices may lead to reduced EV production costs, potentially making EVs more affordable for consumers.

Falling lithium prices pose challenges for lithium battery manufacturers, including declining profit margins and the need for cost-saving measures.

Falling lithium prices may spur innovation in EV battery technology as manufacturers seek to optimize performance and reduce costs further.

The long-term implications of declining lithium prices for the EV industry include increased accessibility, potential growth in EV adoption rates, and reshaping of the automotive market.